mec vec alg ana sta

1 77 82 67 67 81

2 63 78 80 70 81

3 75 73 71 66 81

4 55 72 63 70 68

5 63 63 65 70 63

6 53 61 72 64 73Permutation and Bootstrap Procedures

PSTAT 234 (Fall 2025)

Bootstrap Estimates of Principal Components

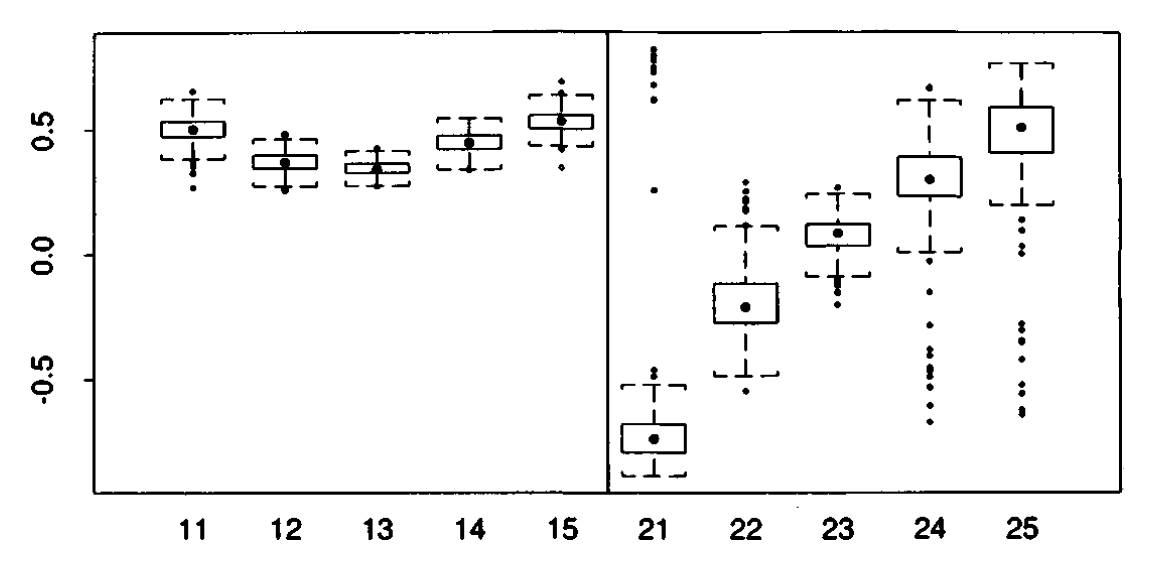

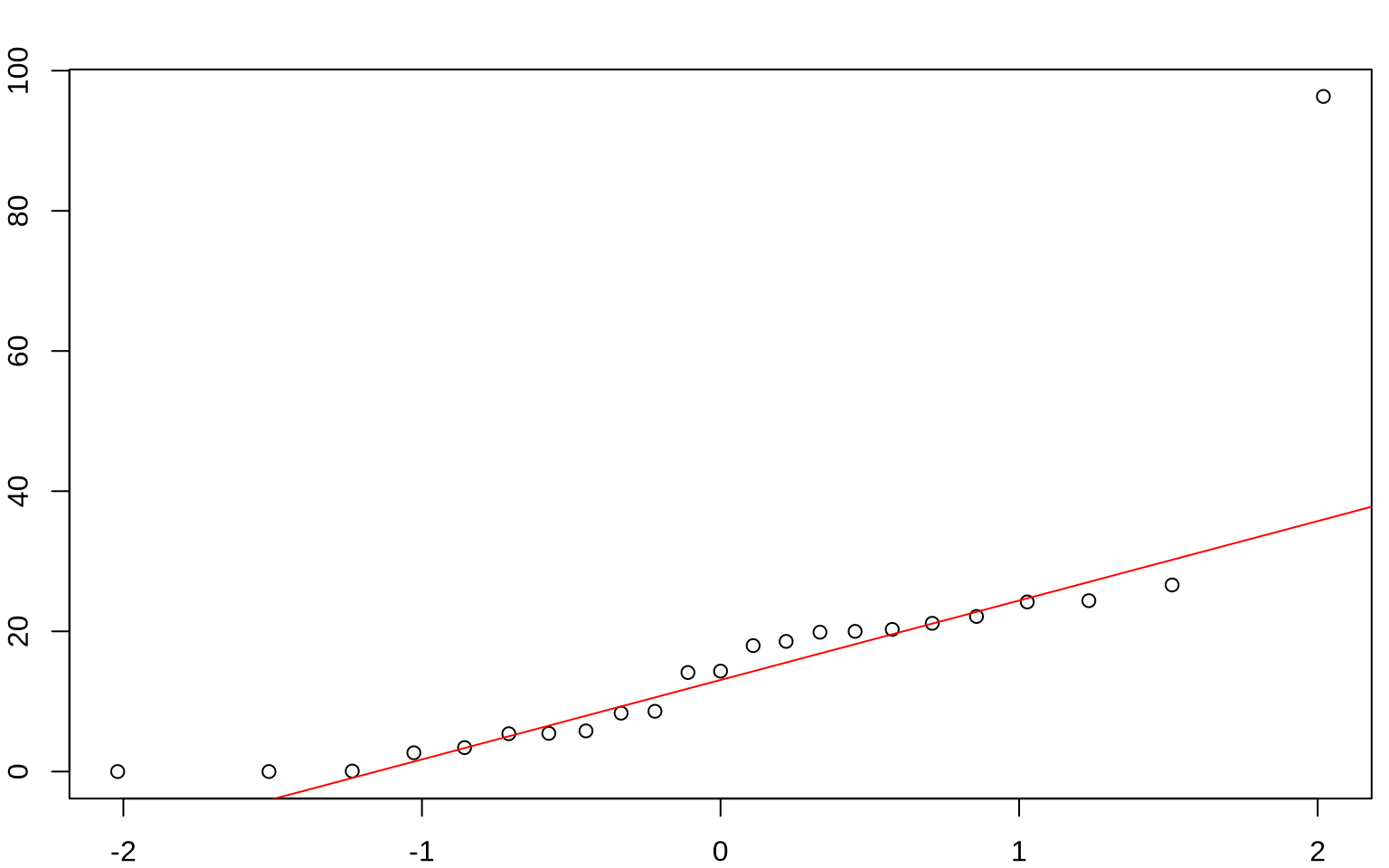

Bootstrap Estimates of Principal Components, \(\hat{\mathbf{v}}_1\) (left panel) and \(\hat{\mathbf{v}}_2\) (right panel) shows empirical distribution of the 200 bootstrap replications \(\hat{v}_{i k}^*\).

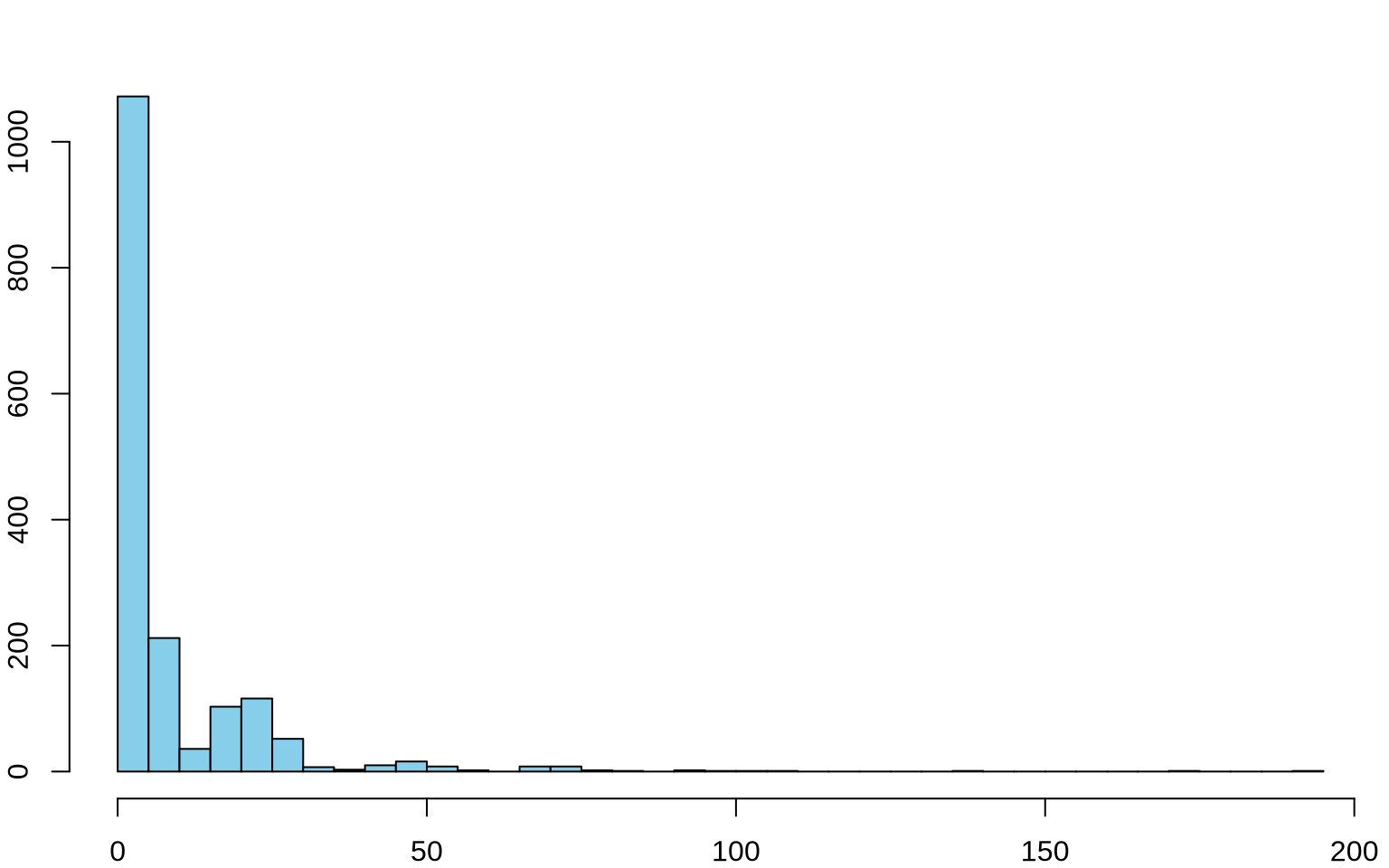

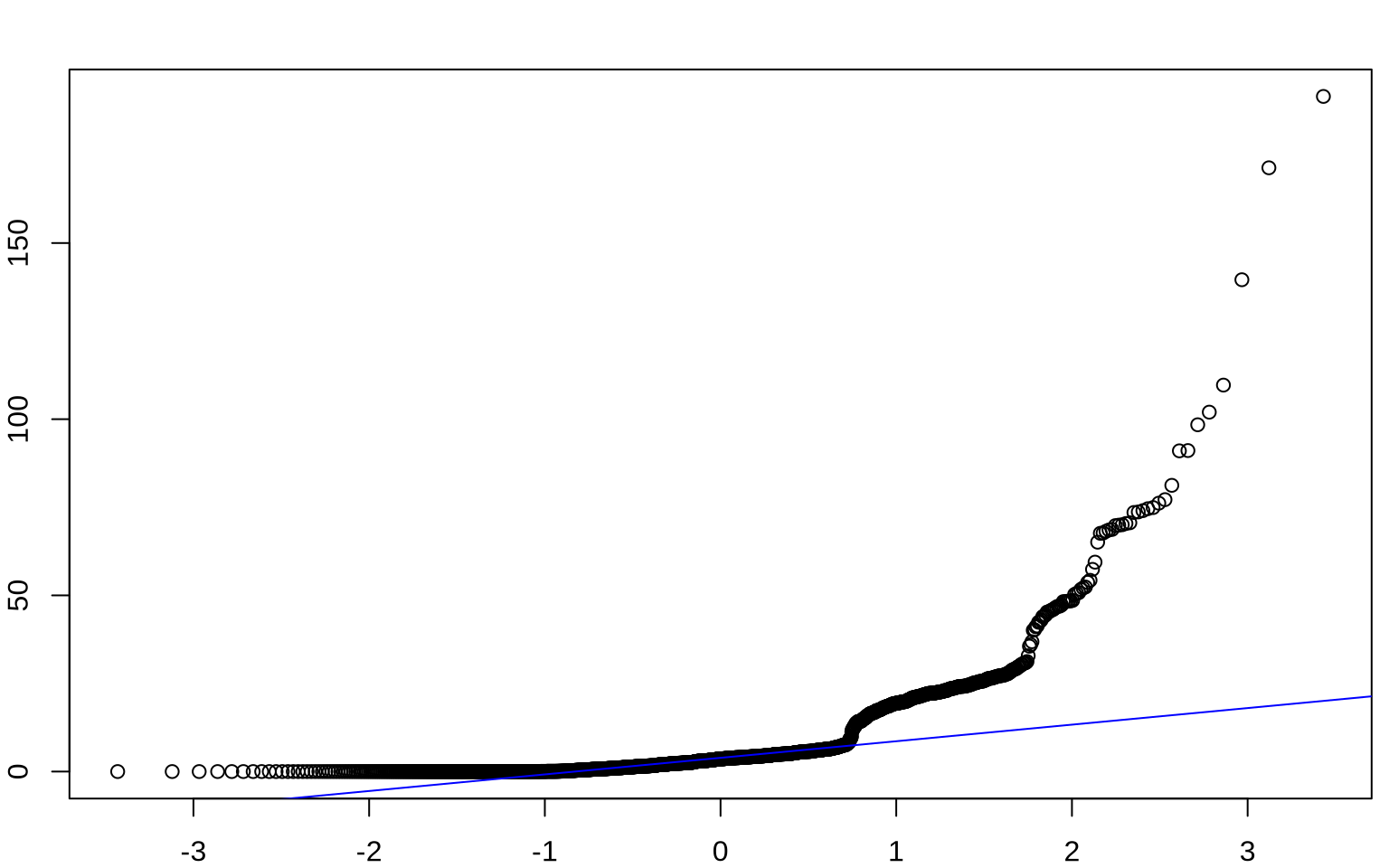

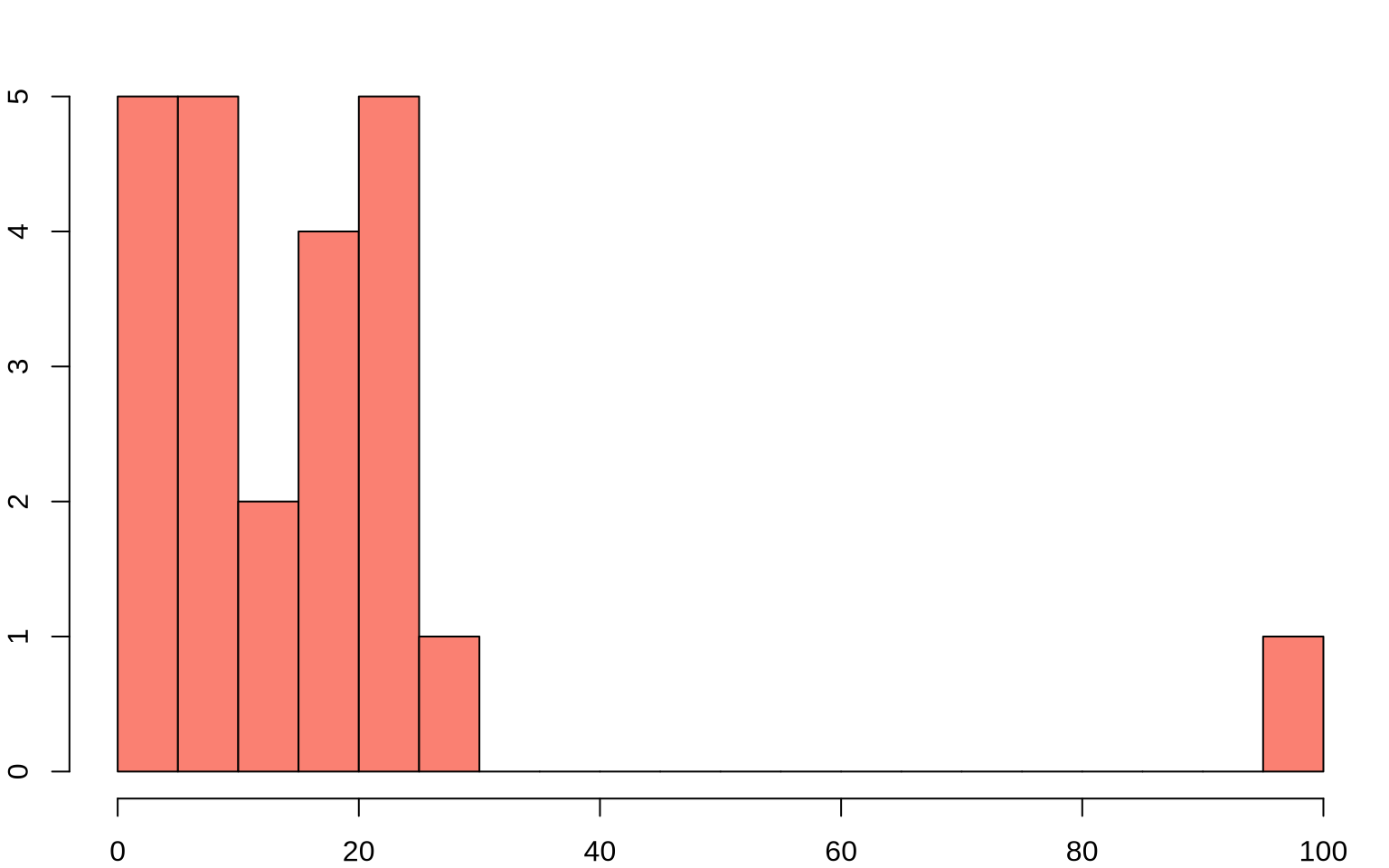

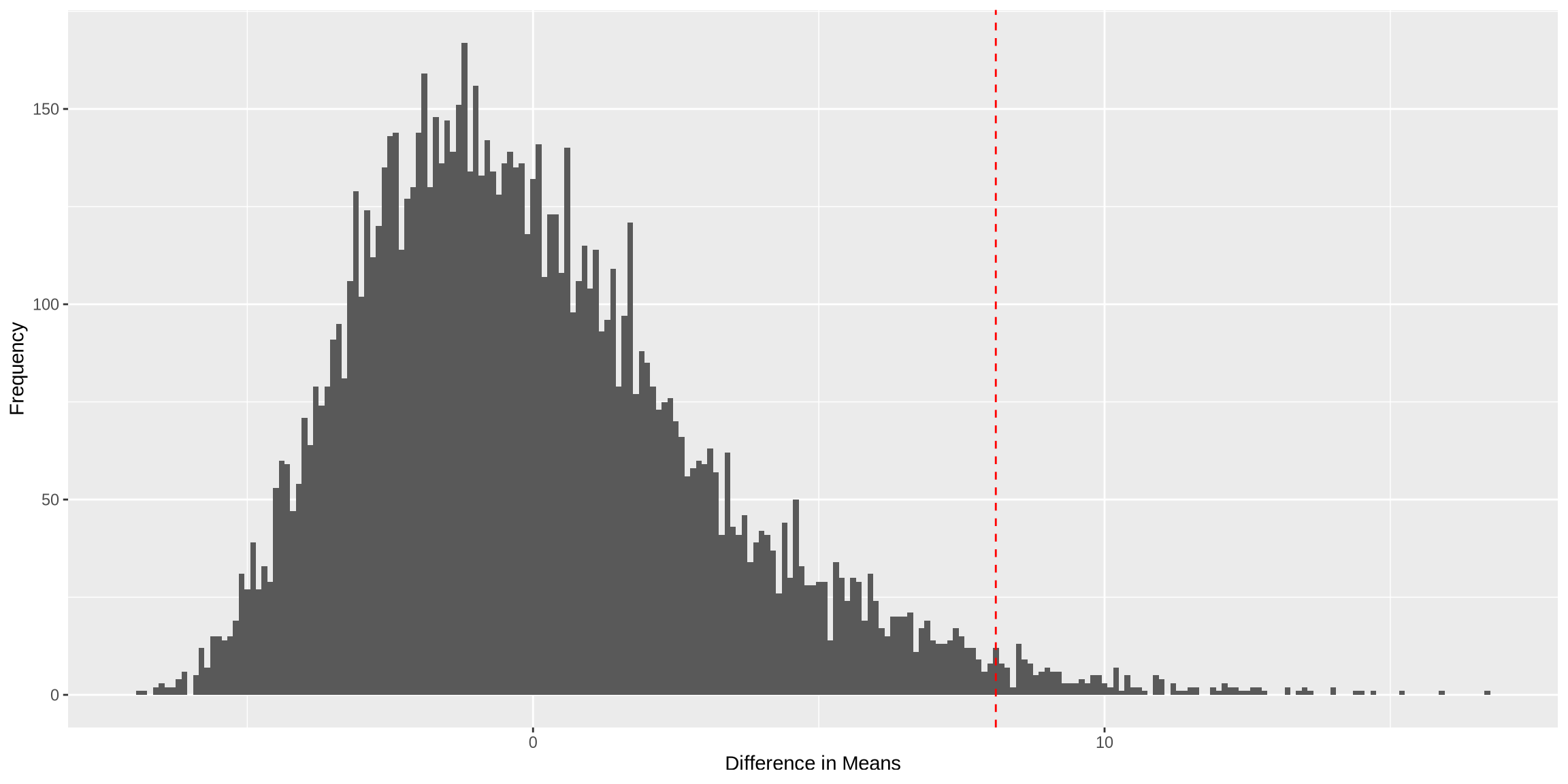

Verizon Data

Permutation Test: Verizon Example

Code

# Calculate the observed difference in means

observed_diff <- mean(CLEC) - mean(ILEC)

set.seed(123)

# Function to perform permutation test

permutation_test <- function(data1, data2, num_permutations = 10000) {

combined <- c(data1, data2)

perm_diffs <- numeric(num_permutations)

for (i in 1:num_permutations) {

permuted <- sample(combined)

perm_clec <- permuted[1:length(data1)]

perm_ilec <- permuted[(length(data1) + 1):length(combined)]

perm_diffs[i] <- mean(perm_clec) - mean(perm_ilec)

}

return(perm_diffs)

}

# Perform the permutation test

perm_diffs <- permutation_test(CLEC, ILEC)

# Calculate the p-value

p_value <- mean(abs(perm_diffs) >= abs(observed_diff))

# Plot the permutation distribution

perm_diffs_df <- data.frame(perm_diffs = perm_diffs)

ggplot(perm_diffs_df, aes(x = perm_diffs)) +

geom_histogram(binwidth = 0.1) +

geom_vline(aes(xintercept = observed_diff), color = "red", linetype = "dashed") +

labs(x = "Difference in Means", y = "Frequency")

| Test | p-value |

|---|---|

| t-test | 0.0299 |

| Permutation | 0.0183 |